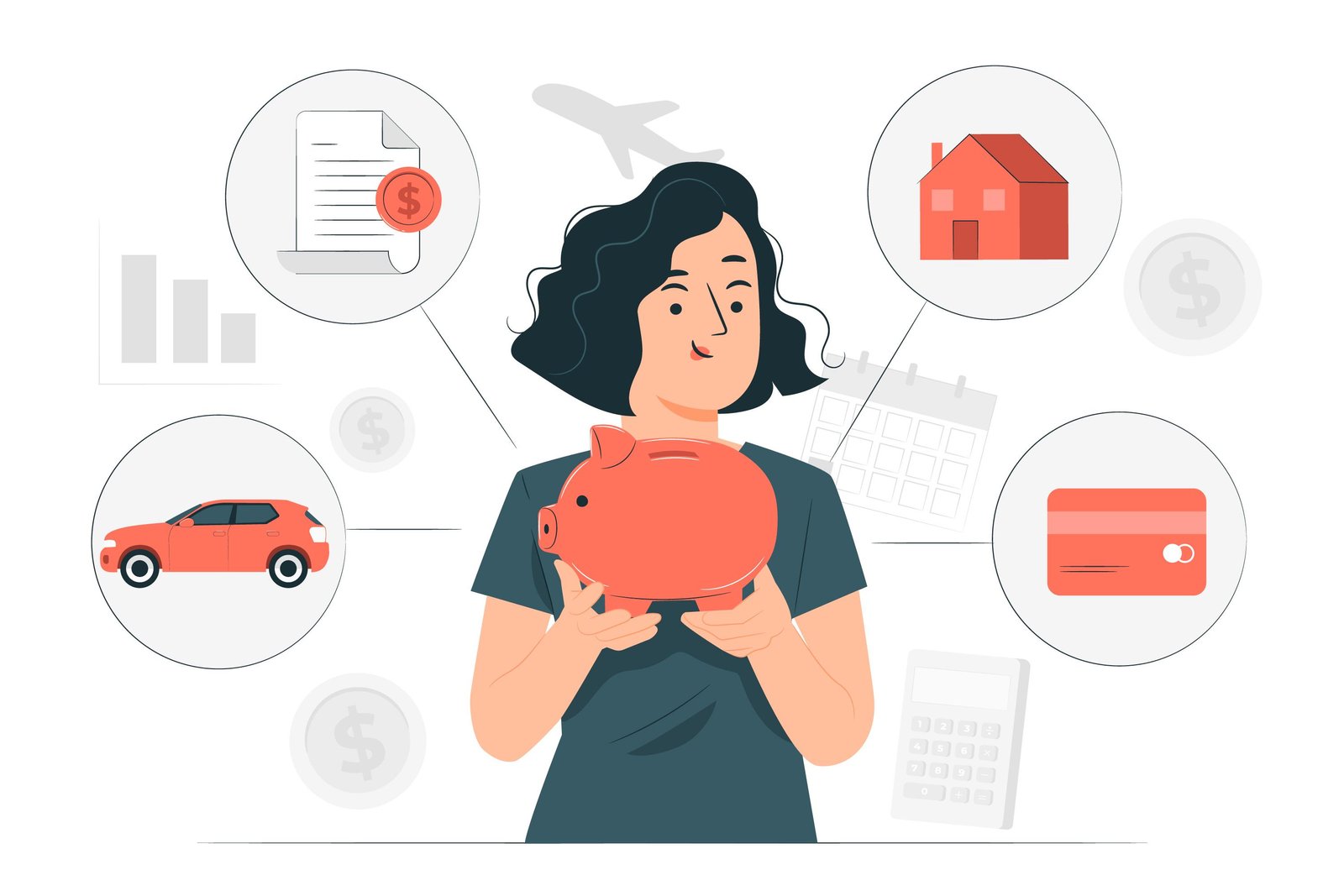

We’ve heard a lot of people talk about generating money, but there aren’t many that talk about managing it properly. Financial management is a difficult subject that many of us deal with. Effective money management helps you to save, invest, and spend your money in a methodical manner, assuring long-term stability and an easy retirement.

Money management, on the other hand, may be done correctly if you follow a few guidelines. Let’s look at some of the top money management strategies in this post.

Set financial objectives.

If you don’t know how to spend your money, there is no way you will be able to save it. As a result, having financial objectives to define how you want to utilize your money in the short and long term is essential. Having these financial objectives provides you more control over your money and helps you to spend it more wisely.

For long-term goals like as purchasing a home or planning for retirement, it is essential that you begin investing your money so that it can increase over time. The goals that you set for yourself should be realistic so that you can achieve then and in return they will keep you motivated.

Create a Budget

Making a budget is a simple chore that plays an important role in your money management journey. People have been creating monthly budgets for years since it enables them to better manage their costs.

When creating your budget, you’ll need to divide your spending into distinct categories based on your goals and requirements. You’ll be able to spend your money more wisely and reach your financial objectives without sacrificing your lifestyle once you’ve set a budget to each area.

Keep Track of Your Spending

After you have completed your budget, the next critical step is to track your expenditures. Tracking your spending may need some effort because you’ll need to go through all of your bank statements, bills, and credit card statements to figure out how much you’ve spent. You may subsequently separate your spending into other categories to determine where you are spending the most and where you might save money.

Examine Your Debt

Many people develop the habit of taking out needless loans and overusing their credit cards, which leads to significant debt. This is exacerbated when a consumer fails to repay it since these items command the highest market interest.

As a result, it is advised that you repay all of your obligations as soon as possible, and if you find it difficult to do so all at once, you may use a debt consolidation loan (with due diligence) to pay off current bills.

Begin Investing Early

The earlier you begin investing, the more wealth you may make over time. It’s fine to start small, but make sure you set aside at least 10% of your monthly income to invest somewhere where it can grow.

Invest in a Variety of Assets

One of the golden laws of investing is to diversify your investments since putting all of your money in one location might result in total loss if the market crashes. As a result, you must invest your money in a variety of assets that will assist you in meeting your long-term and short-term objectives.

Prepare for Emergencies

Emergencies such as medical difficulties and job loss can occur at any moment, therefore it is always prudent to keep some emergency savings on hand. These circumstances frequently cause tension, and in instances like these, not having money can add to the burden. As a result, you must have some emergency cash in order to feel comfortable and prepared for the troubles that may arise in your life.

Save For Retirement

Saving for retirement is one of the most essential things to do, yet many individuals fail to do so. As we become older, our ability to work diminishes, and we must retire at some time in our lives. Many firms have ceased providing pensions, which means you must have some assets on hand if you wish to retire and live a comfortable life.

As a result, if you want to live a tranquil retirement life, it is advised that you begin saving money as soon as possible. You might also consider investing in Real Estate so that the value of your money grows steadily over time. Remember that the more you save, the sooner you can retire.